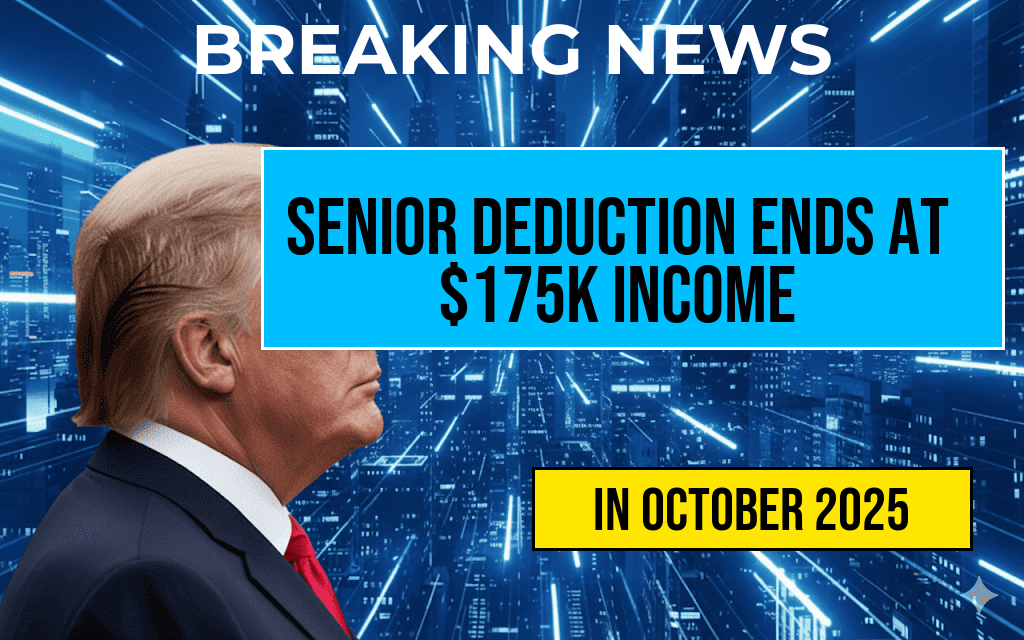

The federal government’s senior deduction, which allows eligible retirees to reduce their taxable income by up to four thousand dollars, is set to phase out for individuals earning more than $175,000 annually. This change, announced in the latest tax updates, aims to adjust benefits in line with rising income thresholds and fiscal policies. Effective immediately, seniors with income exceeding this threshold will see the deduction gradually diminish, ultimately becoming unavailable for those earning above the cutoff. The adjustment reflects ongoing efforts to balance tax relief programs with broader revenue considerations and ensure equitable support across different income brackets.

Understanding the Senior Deduction and Its Role in Retirement Tax Planning

The senior deduction, also known as the age-related tax benefit, has historically served as a crucial component of retirement planning for many Americans. It allows seniors to reduce their taxable income, thereby lowering their overall tax liability. Originally designed to provide relief to those on fixed incomes, the deduction has been a valuable tool for managing tax burdens during retirement years.

Typically, the deduction is available to taxpayers aged 65 and older, with the amount determined by their qualifying income levels. In recent years, policymakers have periodically adjusted the income thresholds to reflect inflation and changing economic conditions. The recent phase-out at $175,000 income signifies a shift towards more targeted support, especially for higher-income seniors who may not require the same level of assistance as lower-income retirees.

Details of the Income Threshold Adjustment

| Income Level | Deduction Eligibility |

|---|---|

| Up to $175,000 | Full deduction available |

| $175,000 – $185,000 | Deduction gradually phases out |

| Above $185,000 | No deduction available |

The phased reduction means that seniors earning between $175,000 and approximately $185,000 will see their deduction decrease incrementally, with no deduction permitted once income surpasses the higher limit. This structure aims to prevent higher-income retirees from disproportionately benefiting from tax relief programs designed primarily for lower-income seniors.

Implications for Retirement Planning

Financial advisors suggest that retirees should review their income streams to understand how this change might impact their tax planning strategies. For those close to the threshold, it may be beneficial to consider tax-efficient withdrawal strategies from retirement accounts or to explore other deductions and credits that could offset increased tax liabilities.

Additionally, the phase-out emphasizes the importance of comprehensive financial planning, especially as tax laws evolve. Retirees earning just below the new cutoff might consider delaying some income or accelerating certain withdrawals to maximize available deductions before the phase-out fully takes effect.

Responses from Policy Experts and Advocacy Groups

Some policy analysts express concern that the adjustment could increase tax burdens for middle-to-upper-income seniors and potentially influence decisions around retirement timing and income management. “While aimed at fiscal responsibility, such thresholds risk complicating retirement planning for many,” said Jane Doe, a senior tax policy analyst at the IRS.

Conversely, advocacy groups argue that the change aligns with broader efforts to create a more equitable tax system. “Adjusting the deduction thresholds ensures that benefits are directed toward those who need them most,” stated John Smith, spokesperson for the National Council on Aging. “It encourages a fairer distribution of tax relief as seniors’ incomes rise.”

Historical Context and Future Outlook

The senior deduction has undergone several modifications over the past decade, reflecting shifting economic policies and demographic changes. As the population ages and retirement incomes diversify, policymakers continue to reevaluate the structure of tax benefits for seniors.

Looking ahead, experts anticipate further adjustments in response to inflation and fiscal pressures. The current phase-out at $175,000 marks a significant step toward recalibrating the program to better align with contemporary income distributions. Stakeholders recommend ongoing monitoring of the impact these changes have on retirement security and tax equity.

For more detailed information on retirement tax benefits and planning strategies, visit Wikipedia’s Retirement in the United States or consult with a qualified financial advisor.

Frequently Asked Questions

What is the Senior Deduction amount currently available?

The Senior Deduction amount is currently set at Four Thousand Dollars.

At what income level does the Senior Deduction begin to phase out?

The phase-out of the Senior Deduction begins when an individual’s income reaches One Hundred Seventy-Five Thousand Dollars.

How does the phase-out of the Senior Deduction work?

As income increases beyond One Hundred Seventy-Five Thousand Dollars, the Senior Deduction gradually phases out, reducing the amount of deductible benefit until it is eliminated at higher income levels.

Will I still receive any Senior Deduction if my income is exactly One Hundred Seventy-Five Thousand Dollars?

No, once your income reaches One Hundred Seventy-Five Thousand Dollars, the Senior Deduction begins to phase out and is typically no longer available at that point.

Are there any exceptions or special rules related to the Senior Deduction phase-out?

Specific exceptions or rules may apply based on individual circumstances or recent tax law changes. It is advisable to consult a tax professional for personalized advice regarding the Senior Deduction.